President/CEO

Warning: Steel prices have started to decline, but no one knows if it'll be a slight retreat and a rapid collapse. Getty Images

With 2022 right around the corner, it’s time to reflect on an unusual and eventful year for the steel industry. Following are Steel Market Update’s Top 10 News Events of 2021:

No. 10—Economy Rebounds from COVID. No one could have predicted when the virus crippled commerce in spring 2020 that the economy would flourish as it has in 2021, leading to record steel demand and record prices.

No. 9—Supply Chain Snarls. A byproduct of the surging U.S. economy, bottlenecks in seaborne shipping, rail, and trucking have led to delayed deliveries of all types of goods, including steel. On the positive side, experts say, this could translate into pent-up demand in 2022.

No. 8—Industry Mergers and Acquisitions Continue. The steel industry continued to consolidate at both the mill and distributor levels as mergers and acquisitions activity heated up. Notable deals included Cleveland-Cliffs’ $775 million purchase of Ferrous Processing and Trading, which made a big splash in the ferrous scrap market. Another example is Reliance Steel & Aluminum’s acquisition of Merfish United, which expanded the giant service center’s reach into the tubular products market, not only in steel but also in copper and plastics.

No. 7—Decarbonization Moves to the Front Burner. Ominous warnings of global warming and its potentially disastrous effects on the environment finally appear to be gaining some political ground. Steel mills, long considered notorious polluters, are now among the many corporate voices touting ambitious goals to reduce carbon emissions from their operations, not only for altruistic purposes but also because customers now demand it. Based on news reports from COP26, the UN Climate Conference just held in Scotland, the challenges ahead to save the planet remain daunting, but international cooperation has never been stronger.

No. 6—Automotive Industry Struggles. Next to construction, automotive is the biggest market for steel. A global shortage of the microchips that are essential to vehicle electronics caused plant shutdowns and production delays amounting to lost sales of some 2 million cars and trucks this year. As a result, there’s an oversupply of automotive-grade steels that could end up on the market, adding downward pressure to steel prices. But once carmakers get the chips they need, production and sales are expected to skyrocket, including surging demand for the new generation of electric vehicles. There is one big caveat: This is all assuming additional parts or material shortages don’t crop up.

No. 5—Section 232 Becomes Trade’s Hot Potato. Ever since President Donald Trump imposed Section 232 tariffs on steel and aluminum imports back in 2018 on debatable “national security grounds,” they have been a source of resentment among trading partners, friend and foe alike. The 25% tariff on steel and 10% tariff on aluminum, however, did reduce competition from foreign suppliers and cleared the way for domestic mills to raise prices to record levels. Trade negotiations have resulted in the removal or modification of Section 232 on several nations and regions, notably Canada, Mexico, and most recently the EU. But the duties remain in place on many big steel-producing nations, such as Russia and Japan. And quotas remain in effect on imports from Brazil and South Korea.

No. 4—Steel Imports Surge. Steel prices in the U.S. rose to such high levels this year that foreign mills could afford to pay the 25% tariffs and still make money. U.S. prices have ranged from $400/ton to $800/ton higher than foreign steel, depending on the product and country of origin. Steel imports jumped by about 37% through the first 10 months of the year. Yet demand has been so strong that domestic prices didn’t really begin to respond to the competition from offshore until the fourth quarter.

No. 3—Mills Reinvest the Windfall. Virtually all the publicly held companies in the steel industry reported record sales and profits this year because of the historically high steel prices. To their credit, most have announced plans to reinvest the windfall in new and upgraded production facilities. The list of projects is too long to detail here, but the investment is expected to result in an estimated 23 million tons of steelmaking capacity in North America, offset somewhat by idlings and closures of older mills.

No. 2—President Joe Biden’s Infrastructure Bill Becomes Reality. After months of debate and political infighting, Congress was finally able to pass long-needed infrastructure funding that stands to be a boon for the steel industry. The measure includes funding for about $850 million in steel-intensive projects that will upgrade the nation’s roads, bridges, rail, ports, and electrical grid. That equates to as much as 40 million to 45 million tons of new steel demand over the life of those projects, according to industry estimates.

It’s been a wild ride for hot-rolled coil prices over the past 14 months. It looks like the peak has been reached, but many market observers are expecting a volatile period for steel prices in the early parts of 2022.

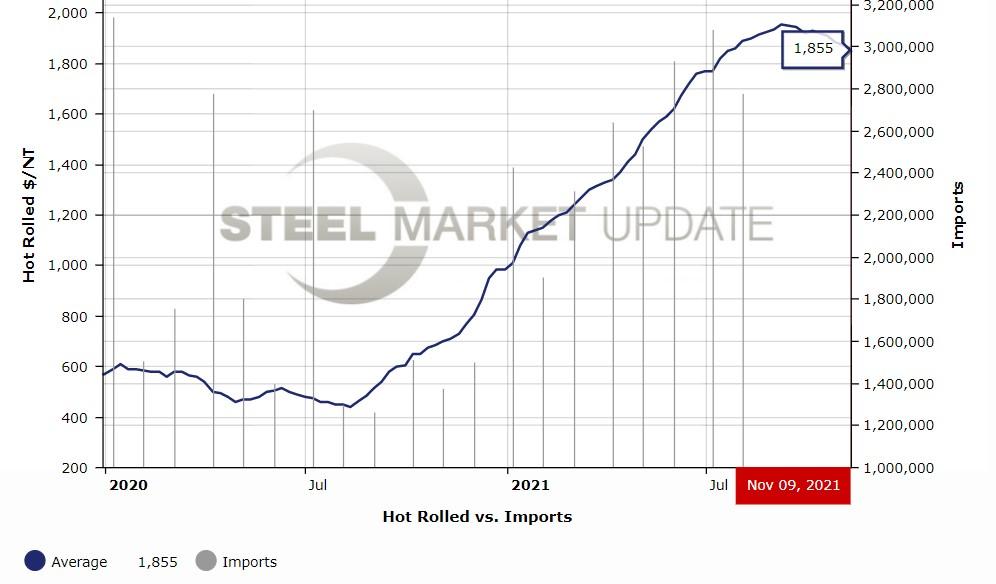

No. 1—Steel Prices Make History. Observers can debate the order of the ranking above, but no one will dispute that steel prices have dominated the headlines in 2021. Fueled by trillions in government stimulus to keep the economy from succumbing to the fallout from COVID, steel demand far exceeded supply for most of the year. The benchmark price for hot-rolled steel quadrupled, from less than $500/ton to a peak of $1,955/ton, in a September-to-September comparison. Steel prices are likely to be the top story again in 2022 as the market waits anxiously for an expected correction.

Hot-rolled coil (HRC) steel prices have peaked and are on a downward trajectory. The question on everyone’s mind: How far and how fast will prices decline?

Steel Market Update (SMU) surveys steel buyers every week. In SMU’s questionnaire on Nov. 11, we asked: Where will hot-rolled prices end the year? Half of respondents predicted $1,800/ton or higher, the other half from $1,800/ton to as low as $1,600/ton.

Let’s put those numbers in perspective. SMU’s check of the market in the week of Nov. 8 put the average price for hot-rolled coil at $1,855/ton. That’s where it was in July and down about $100/ton from the market’s apparent peak of $1,955/ton in early September. If the market continued to move lower at the same rate, that would put the benchmark price of HRC just below $1,800/ton by year’s end, or a correction of around 8%. Doesn’t sound like much, but in a normal market with HRC around $600/ton, a sudden drop of more than $150/ton would be considered a disaster.

And what if the pundits are right and steel prices plunge? On the way up, it was not uncommon for HRC prices to jump by $30/ton to $40/ton in just a week. It’s not inconceivable the same could happen on the way down, though that appears unlikely at this point.

With hot-rolled prices on the escalator down and cold-rolled and coated prices basically marching in place, steel buyers are worried and confused. One-third of the service center and manufacturing executives polled last month said they are sitting on the sidelines waiting to see how prices play out before committing to purchases for inventory.

With steel prices having peaked and people wondering what’s next, steel buyers are an anxious lot. Here are some of the comments that steel buyers recently shared with SMU:

SMU’s popular “Steel 101: Introduction to Steel Making & Market Fundamentals” workshop will be held virtually next month, Jan. 11-12. Information on the agenda, instructors, and costs is available here.

SMU’s “Introduction to Steel Hedging” workshop also is a virtual event covering techniques to protect your company and customers from steel price volatility. The next session is scheduled for Feb. 1-2. More information is available here.

The 33rd Tampa Steel Conference, an in-person event, will be held at the Marriott Water Street Hotel in Tampa, Fla. You can learn more about the agenda, speakers, costs to attend, and how to register by visit this page.

The Fabricator is North America's leading magazine for the metal forming and fabricating industry. The magazine delivers the news, technical articles, and case histories that enable fabricators to do their jobs more efficiently. The Fabricator has served the industry since 1970.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

In this episode of The Fabricator Podcast, Caleb Chamberlain, co-founder and CEO of OSH Cut, discusses his company’s...