President/CEO

Steel prices, which have climbed for the better part of a year, appear to have reached their peak. Getty Images

When the books are written on a historic year for steel prices, we will probably look back at August and September as the months when things started falling apart.

Recall that over the summer prices continued to soar upward, and consensus seemed to be not whether hot-rolled coil (HRC) prices would breach $2,000/ton ($100/cwt), but when. The new consensus, according to Steel Market Update (SMU) survey respondents, is that prices already have peaked or will peak before the year is out.

And SMU’s HRC prices reflect that trend too. SMU’s average HRC price was at $1,920/ton as of Oct. 11, down $35/ton a month earlier. September also saw prices decline for three consecutive weeks—the first time that had happened since the market buckled under the weight of the pandemic in the summer of 2020.

What the heck happened? Not to toot SMU’s horn too much, but we called this one back in September. Prices were still moving higher then, but the writing was on the wall. There were a lot of gaps to close—between domestic and foreign prices, between steel and scrap prices, and between market sentiment and reality (as measured by lead times). Such unprecedented spreads could not hold unless a new precedent were established, and to date, one hasn’t been.

Let’s take the gaps in order. First, imports.

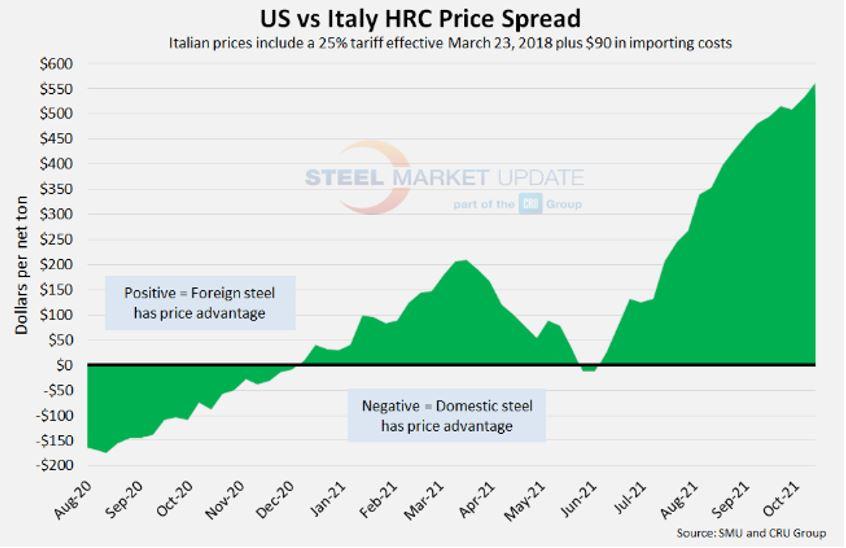

The spread between import prices and domestic prices had reached its widest point ever by the end of September. U.S. prices were theoretically about $850/ton more than Asian HRC prices, and that premium was approximately $400/ton to $500/ton compared to EU prices. Take for example Figure 1, which shows HRC prices in Italy compared to those in the U.S.

That initially enticed people near coastal areas, where imports are always a bigger part of the mix. Transportation is expensive and ports congested, but with discounts of hundreds of dollars per ton, many buyers calculated that the gap between foreign and domestic prices made imports worth the risk.

And it wasn’t just coastal buyers. We’ve contacted people in the Ohio Valley who were buying foreign material, shipping it upriver, and still seeing significantly lower prices on a delivered basis compared with what domestic mills were offering on FOB terms.

Because of this, the U.S. has been importing at least a steel mill’s worth of extra production every month, sometimes almost the equivalent of two mills’ production. This has been going on for a while now.

Some back-of-napkin math confirms this. The new sheet mills announced by Nucor and U.S. Steel will have annual capacity of 3 million tons/year, or 250,000 tons/month. Flat-rolled imports have totaled 1 million short tons or more every month since May, and the figure has been 1.2 million to 1.3 million short tons since August, according to U.S. Department of Commerce figures. That’s 200,000 to 500,000 tons more than the monthly average of approximately 800,000 tons over the last two years.

Figure 1. Hot-rolled coil from Italy has had a substantial price advantage over domestic steel for most of 2021.

Our latest channel checks indicate that many buyers are continuing to load up on foreign steel.

We know a lot of people were making the case that any correction would be gradual. Here’s another reason why we thought that didn’t make sense.

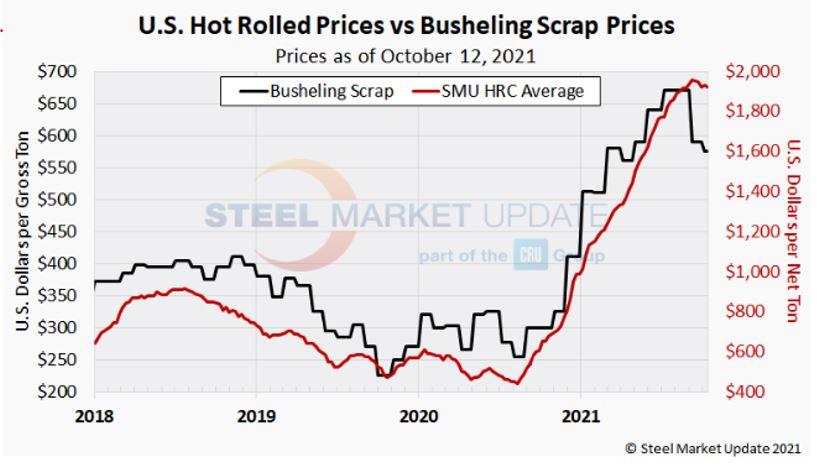

Take a look at the gap between HRC prices and prime scrap prices (see Figure 2). An old rule of the thumb is that conversion costs from scrap to coil are about $150/ton, maybe $175/ton in a slow market when mills are running below capacity and therefore less efficiently.

Take the current price of HRC and add $150/ton to $175/ton. That’s roughly the break-even point for domestic electric arc furnace (EAF) sheet mills. And that gives you some idea of how far prices could fall in the transition from a market in which mills could name their price to a market with a more traditional cost-plus model.

We’ve written elsewhere that over the past year scrap prices took a daytrip to the Indiana Dunes and steel took a mega-yacht to Tahiti. The bill for those trips is now coming due. The trip to the South Pacific cost a lot more than the side trip to the Indiana.

How can we be so sure of that? Because we’ve seen this movie before. Think back to Q2 2018, when Section 232 tariffs were unexpectedly rolled out not only on U.S. adversaries but also on trading partners and allies like Canada, Mexico, and the EU. Steel prices shot upward even as scrap prices stayed comparatively steady. But steel prices fell in 2019 when tariffs were removed from Canada and Mexico.

It now appears likely that Section 232 tariffs on the EU will be replaced with a tariff rate quota (TRQ), a mechanism under which imports below a certain volume would not face tariffs. A TRQ would have an impact, given the price differential mentioned above and considering that European steel is high quality and can reach the U.S. a lot faster than material from Asia.

Speaking of Asia, what will Japan say if the EU gets a new deal. Won’t they want one too?

Domestic mills have talked a lot about discipline over the last year, but discipline is easy when the market is going up. It will be tested as prices move lower.

U.S. mills might undercut one another to attract business, or they might try to undercut imports. U.S. EAFs are very low cost, and some EAF steelmakers have explicitly stated that their new capacity is intended to displace imports. They will be able to do that, but only if they become price-competitive with foreign steel and if they narrow the steel-scrap gap.

Figure 2. Scrap prices remain high, but industry observers agree that trend won’t continue given the downward pressures being applied to domestic steel prices.

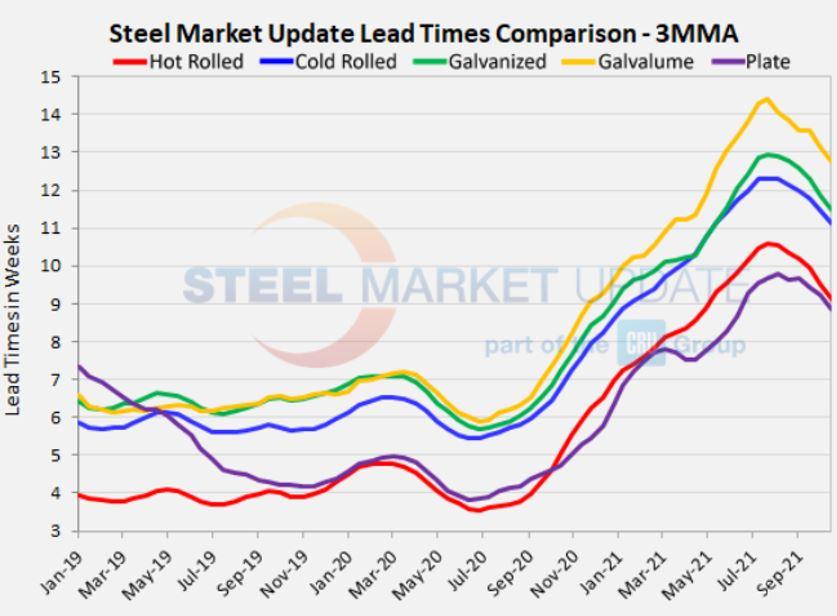

Another gap that seems unsustainable is the one between lead times and market sentiment. Lead times, the time between when an order is placed by a mill and when that order is produced, are typically an advance indicator of pricing direction. When lead times are stretching out, it typically means prices are going up or soon will. The opposite is also true. When lead times are getting shorter, it typically means prices are falling or soon will.

In recent months, lead times have been getting shorter (see Figure 3).

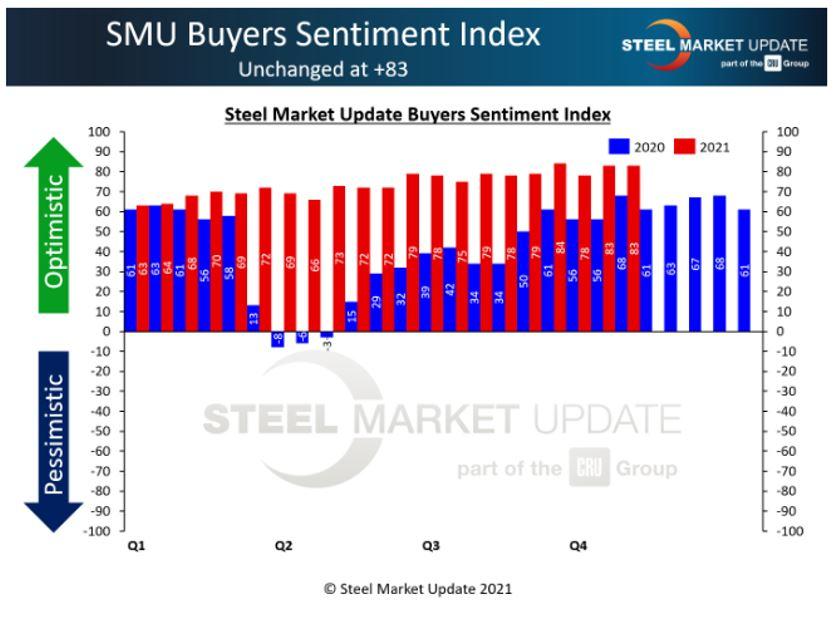

In contrast, SMU’s Steel Buyers Sentiment Index, a measurement of how North American flat-rolled steel market participants feel about their companies’ prospects, has been at or near record highs (see Figure 4) even as steel prices and lead times have fallen.

Sentiment last dropped into pessimistic territory following the COVID-19 outbreak. It has been solidly optimistic ever since.

It’s unusual to see record-high sentiment and shorter lead times. The two indicators typically trend together. But we’re hoping this particular gap doesn’t close.

The spreads between domestic prices and import prices need to close for the U.S. market to remain competitive, and that necessarily implies a narrower spread between steel and scrap prices.

What we’re hoping is that the strong readings we’ve had on sentiment mean that demand, unlike prices, is still on firm footing and will remain so even as prices normalize.

What’s one to do in volatile times? Tune into SMU’s next “Introduction to Steel Hedging: Managing Price Risk Workshop” on Nov. 2-3. The event will be virtual. You can learn more about the agenda and register by visiting here.

If you’re looking for an in-person event, check out the Tampa Steel Conference, which is co-hosted by SMU and Port Tampa Bay. The event will be held on Feb. 14-16, 2022, at Tampa’s Marriott Water Street Hotel. You can learn more by visiting here.

The Fabricator is North America's leading magazine for the metal forming and fabricating industry. The magazine delivers the news, technical articles, and case histories that enable fabricators to do their jobs more efficiently. The Fabricator has served the industry since 1970.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

In this episode of The Fabricator Podcast, Caleb Chamberlain, co-founder and CEO of OSH Cut, discusses his company’s...

{kind=link}