President/CEO

Steel prices have reached record highs and lead times are increasing. Reports indicate that some service centers are turning away spot buyers because they simply don't have the inventory. Getty Images

Steel prices just keep moving higher and higher. At some point, prices will get too high, and fabricators and manufacturers will stop buying. Demand will stall. Or so goes the conventional wisdom. But it hasn’t happened yet, and it may not this year.

Steel Market Update (SMU) polls steel buyers every week to keep tabs on market conditions. As of mid-April, few reported any signs of high steel prices eroding demand. Half said demand was stable. And more than 40% said demand for their products and services was growing. Only 6% reported declining demand. Here’s what a few of them had to say:

SMU also asked: “Have you seen any indications that record-high steel prices might be near a tipping point?” The vast majority, nearly 80%, reported no signs of a change in the market’s direction. Some of their comments were:

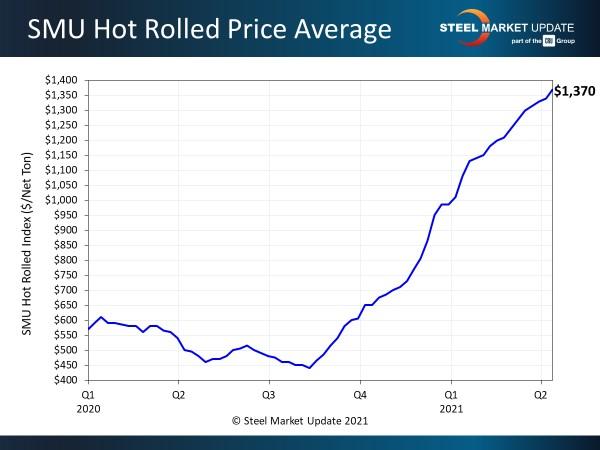

SMU’s survey of the market on April 12-14 revealed a benchmark price for hot-rolled coil (HRC) of $1,370/ton (see Figure 1). That’s incredibly high. It also was almost entirely unexpected so close on the heels of a black swan event like the pandemic. HRC prices have set new highs week after week since January as the economy recovered from the pandemic. At $1,370/ton, HRC is selling for triple its 2020 low of $440/ton, which occurred last August. That price also is $300/ton more than the previous supercycle for commodities in 2008. (A supercycle occurs when supply for a commodity is so inadequate when compared to demand growth that prices rise for an extended period of time.) Cold-rolled and coated steel prices have experienced similar inflation.

Why the runup in steel prices? Simply put, an imbalance between supply and demand. When the economy shut down last spring to stem the spread of the coronavirus, steel demand plummeted, and mills idled capacity. Fueled by government stimulus, the economy and steel demand have come roaring back. But steel production has not. Steelmakers have taken advantage of the situation to conduct much-needed maintenance on furnaces and other equipment, and it appears they are in no hurry to correct an imbalance that is delivering record profits

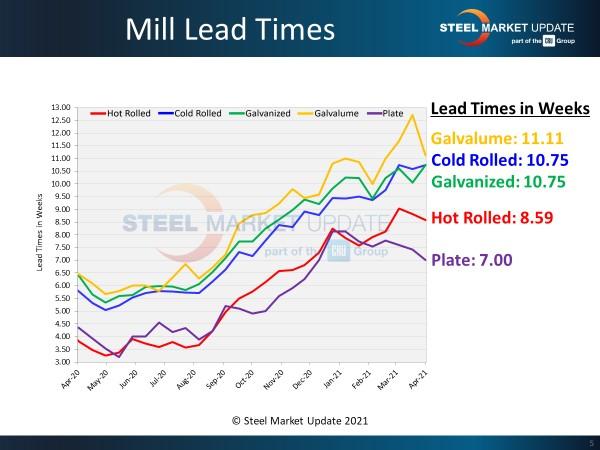

.Buyers have told SMU that almost all the steel being produced is for contract customers and that the few spot tons available are selling at a huge premium. Mills’ lead times have extended to more than eight weeks for hot-rolled and nearly 11 weeks for cold-rolled and coated products—more than double traditional lead times (see Figure 2).

Service centers are operating with record-low inventories—an average of just 1.8 months of supply at the end of March, according to SMU’s proprietary data. That’s more than six inventory turns per year, far leaner that the normal four turns. Most service centers would welcome the opportunity to buy more steel if it were available. Because they cannot get more tons, some have had to turn customers away.

SMU also regularly asks buyers to predict when and at what level steel prices will peak. In every instance since late last year, the consensus view has been wildly incorrect. Namely, buyers consistently agree that a peak is nearby, and then prices continue to march significantly higher. So take the following with a grain of salt: As of mid-April, the prevailing view was that hot-rolled prices would continue rising to at least $1,400/ton. About half of the buyers contacted by SMU predicted that prices would at last lose their upward momentum by June. The reason: additional domestic capacity colliding with increased import volumes. But almost as many, around 38%, said it might be well into the second half before steel prices moderate as supply catches up with demand. Here are some buyers’ comments:

It’s important to note that considerable additional supply is in the works. Big River Steel has fired up a second electric-arc furnace at its mill in Osceola, Ark. JSW USA has restarted its EAF in Mingo Junction, Ohio. Union members are now back to work at the NLMK USA mill in Farrell, Pa., following a lengthy strike. Steel Dynamics Inc. is on track to begin production at its new mill in Sinton, Texas, sometime this summer, as is Ternium in Mexico. A large volume of imports also is forecast to begin arriving in the U.S. this summer and into the fall.

But the demand side of the equation also is in flux. The U.S. economy is booming thanks to the government stimulus to counter the pandemic. Positive weather in most of the country has gotten the construction season off to a good start. Automakers have been hobbled by a worldwide shortage of microchips, which is likely to push some vehicle production into the second half of the year. And the Biden administration is pushing for trillions in new infrastructure spending, though most of that work and steel consumption won’t manifest until 2022 and beyond.

Figure 1. Prices for hot-rolled coil continue to climb well into April, and many steel buyers think it might not end there.

Where and when supply and demand will meet in the middle remains a puzzler, one with big consequences for steel buyers.

Presuming COVID inoculations continue apace, the annual SMU Steel Summit Conference will be in person Aug. 23-25 at the Georgia International Convention Center in Atlanta. Visit www.events.crugroup.com/smusteelsummit/home for more information.

To sign up for a free trial of SMU’s newsletter, contact paige@steelmarketupdate.com.

The Fabricator is North America's leading magazine for the metal forming and fabricating industry. The magazine delivers the news, technical articles, and case histories that enable fabricators to do their jobs more efficiently. The Fabricator has served the industry since 1970.

start your free subscription

Easily access valuable industry resources now with full access to the digital edition of The Fabricator.

Easily access valuable industry resources now with full access to the digital edition of The Welder.

Easily access valuable industry resources now with full access to the digital edition of The Tube and Pipe Journal.

Easily access valuable industry resources now with full access to the digital edition of The Fabricator en Español.

In this episode of The Fabricator Podcast, Caleb Chamberlain, co-founder and CEO of OSH Cut, discusses his company’s...

{kind=link}